Can you afford to buy a home and pass the mortgage stress test? It’s a big question, and I want you to answer it without the bias of banks, lenders, family, or friends swaying your decision. Heck, you may have some bias knocking your noggin too because home ownership can be a built-in dream or expectation for many.

So to keep you from being house-poor, I’m giving you some information-rich thinking with a little math and a lot of logic. These five steps and one spreadsheet could save you much money and a lot of grief when looking to buy a home. Also, check out my segment with CBC’s On The Money for my words in action.

Peter Armstrong and I also did a VERY popular Facebook live on housing affordability, so be sure to check it out too.

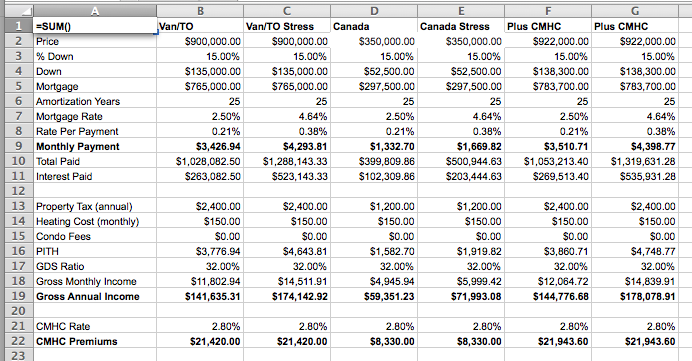

Step 0. Get the Housing Affordability Calculator

I made a bias-free quickie spreadsheet to show you the impact of rising interest rates on your mortgage payments. I know it’s nerdy and unsexy, but it’s real and it works. So download the darn thing and plug and play with YOUR OWN money numbers at will to see if home ownership is right for you. There’s even a cell for showing the impact of CMHC insurance premiums on your monthly payment — something that’s uncommon out there. So take the free tool and use the information.

Download: Housing Affordability Calculator

Step 1. Stress Test your Emotions

Why do you want to buy a place? I want you to check your emotions at the door before you buy the door.

FOMO is not a solid financial strategy.

Is a FOMO (fear of missing out) panicking you into the market? FOMO is not a solid financial strategy, so don’t let super hot markets (like those in Vancouver or Toronto) push you into a property if you’re neither financially nor emotionally ready. If you’re fearful of being “priced out” of home ownership, calm your emotions — if you can’t afford a place today chances are you won’t tomorrow when interest rates rise. So stay out of the market until your fear is replaced with a sensible downpayment and a market that is more favourable to buyers.

Speculating on speculation.

If you think you’re investing in a property because you can always sell that property to someone else at a greater price, you’re not investing — you’re speculating. If that’s your play, then good luck ’cause when the music stops you want to be the one holding the money and not the house. Don’t gamble your family home, OK?

Home sweet home for a decade, or more?

Looking to build a life, grow some roots, and stay for a while? If you love the community, have researched the place, and plan to live in your new space for 10 years or more, chances are you can weather a few real estate dips and won’t get taken in the short term by all the fees and expenses associated with selling a home. Now we’re talking, so let’s move on to stress testing your finances.

Step Two: Mortgage Stress Test Mortgage

Money is a house-keeping item. Without it, you can’t keep your house.

Back in 2016, Ottawa introduced a Mortgage Stress Test to prevent prospective homebuyers from making the biggest financial mistake of their lives by protecting them from rising interest rates. Those with less than 20% down on the purchase price of a home (a high-ratio mortgage) must qualify at both a current rate and at a higher rate, around 2% more. If today’s rate is 2.5%, lenders would test mortgage payments at the Bank of Canada’s qualifying five year fixed rate of 4.64%. Got it? The idea is, basically, in a nutshell, can you still afford your home when rates go uppity up!

A general borrowing rule of thumb is a mortgage should not exceed 3X your annual income. So if you earn $75,000 per year, your mortgage should be maximum $225,000. The challenge for buyers in hot markets like Toronto and Vancouver, is homes now cost 7✕ to 8✕ the average gross income.

The reality is there is little room for interest rates to decrease and even a modest rate increase will drive up mortgage payments significantly. Can you afford it? Whether you have 20% down or not, it’s prudent to stress test your mortgage payments at higher interest rates to stay financially safe. Be smart, don’t be stressed.

Let’s take a look at two Stress Test scenarios. First, the Toronto/Vancouver scenario and then the more sane markets in Canada.

Example: Toronto/Vancouver Stress Test Mortgage

The Details: A 900K house with 15% down (135K), 2.5% interest rate.

Assuming: $2400 annual property taxes, $150 heat/month.

Total monthly cost: $3,776

Gross income required: $141,635

Now the Stress Test:

Stress Test Rate: 4.64% (keeping the rest the same)

Total monthly cost: $4,643

Gross income required: $174,142

Bottom Line: On a 900K house with 15% down, your payments jump $867 per month while your gross annual income must increase by $32,000 to pass the stress test.

Example: Canada Housing Stress Test

The Details: 350K house with 15% down (52.5K), 2.5% interest rate.

Assuming: $1200 annual property taxes, $150 heat/month

Total Monthly Cost: $1,582

Gross Income Required: $59,351

Now the Stress Test:

Stress Test Rate: 4.64% (keeping the rest the same)

Total monthly Cost: $1,919

Gross Income Required: $71,993

Bottom Line: On a 350K house with 15% down, your payments jump $337 per month while your gross annual income must increase by around $12,500 to pass the stress test.

Are you feeling the pinch of the simple stress test stuff? Now let’s look at the stuff the bank doesn’t tell you.

Step Three: Don’t forget about CMHC Insurance!

Don’t forget the Canadian Mortgage and Housing Corporation (CMHC) premiums when determining your mortgage payments! With less than 20% down, borrowers have to pay this unfun thing called mortgage default insurance, or CMHC insurance, or kick you in the butt when you’re already feeling down premium.

CMHC insurance is mandatory in Canada for down payments between a minimum of 5%, up to 19.99%. The real kicker is this mortgage default insurance only protects lenders in the event a borrower (you) defaults on the mortgage. The money you’re paying does not protect YOU, kind borrower. And since nothing excites a lender more than risk-free lending, you betcha you’d better be diligent and account for this premium in your Stress Test when scraping together a downpayment of less than 20%.

I looked around the CMHC website and various lenders to see if including CMHC Insurance within the Stress Test was a normal and (very transparent) thing. I found nothing. So I called the CMHC to get their take. Here’s the response:

CMHC: “Unfortunately it’s not written on our website. It won’t specify it on the website. Usually the lender should mention that premium.”

WHAAT? OK, how about I mention that premium.

On our 900K house with a 15% (that’s 135K) down payment, the CMHC premium is 2.8% of the total loan.

$900K – $135K = $765K

$765K ✕ 2.8% = $22,000 CMHC premium.

Yes, on that 900K house, you’re paying $80 more per month on your mortgage payments to cover the CMHC premium which only covers your lender’s butt.

Step Four: Never take a lender’s word for it.

Lenders get paid to lend. Lenders want you to borrow as much as you’re willing to take. So never EVER take a lender’s word for it that you can afford a home.

Along with the “Mortgage Stress Test”, lenders use two metrics to determine how much you can borrow. One is the Gross Debt Service Ratio (GDS), the other is the Total Debt Service Ratio (TDS). I’ve listed both metrics below.

The problem with these ratios is both use your gross income (amount you make BEFORE taxes) to test your ability to afford a mortgage. WHAAAT? Since you don’t get to keep all your income (the government takes a chunk), these metrics can put the borrower (you) at a loss because you only keep your net (after tax) income to cover life’s costs. The lender doesn’t have to struggle with the shortfall. You do.

Another issue is the TDS accounts for your debt, but fails to calculate saving money for the future, such as your retirement (RRSP, TFSA), your kid’s education (RESP), or if you can afford a new heating system if your current system conks out. These metrics also fail to consider your life when determining your eligibility. So if you have daycare costs, disabilities, future illness, or job loss down the road, your lender does not have a metric to give you a financial safety net to keep you financially safe in your house.

Here are the metrics that make me mad:

GDS: Gross Debt Service Ratio

= (Monthly House Cost) ÷ (Gross Monthly Income)

= (Mortgage + Property Taxes + Heating + 50% of condo fees) ÷ (Gross Income)

Guideline: Maximum GDS 32%

Allowed: Maximum GDS 39%

TDS: Total Debt Service Ratio

Similar to GDS, but includes other debt servicing too:

= (House Cost + CC interest + Car Payments + Loan Expenses) ÷ (Gross Income)

Guideline: Maximum TDS 40%

Allowed: Maximum TDS 44%

Bottom Line: The bank or lender gives you an upper bound you can borrow. Ignore it. It’s most often better to borrow LESS. Tally your AFTER TAX income, subtract your AFTER tax savings and that number tells you how much you can borrow. Also add a Stress Test buffer to your calculation in case interest rates rise.

Step Five: If you’re “priced out” of the market – STAY OUT!

Markets go up, markets go down. NEWSFLASH: This housing market is not your market. Housing affordability is at an all time low in some cities and areas in Canada. You’re not alone.

Use math, not emotion when making the biggest financial decision of your life. FOMO is a temporary emotion, but buyer’s remorse could financially last a lifetime.

Love love love,

Kerry

Thank you so much for this. All those who want to purchase a home should read this and follow the steps before making a decision. Ignore them at your peril.

Buying a home is very emotional. It’s great you put it forward. But FOMO is only one emotional argument. How about fear of remaining a tenant? Why does renting have a negative perception?

The rent market can be now very interesting for the younger generation, very mobile and looking for better location than ownership.

You know, you can buy a HOUSE; ‘homes’ have to be made…

Yes, take your time. We finally bought during the last down turn. Life stress tested us but we are still getting by. So glad we didn’t buy a bigger house.

I think home ownership has become a priveldge and not a right anymore.

renting is not a bad thing if you can find a place that will allow you some freedoms . examples having a pet or a child or hanging clothes to dry. Some places have very restrictive rules.

Hi Kerry, Great Article!

I’m just a little confused by the following under TDS: Total Debt Service Ratio”

“Allowed: Maximum GDS 44%”

Is this a typo? Should it read “TDS 44%” ?

Thanks

Hi Michelle, Thanks for finding the typo! All fixed! Cheers, Kerry

For the mortgage rule of thumb – is that 3 x your net or gross household income?

The mortgage rule of thumb often cites gross income — your income before paying taxes.